Deliver more than general advice—deliver tailored, industry-specific guidance that positions you as an indispensable part of your clients’ success. Vertical IQ arms you with the Industry Intelligence, relevant talking points, risk analysis and proprietary economic and local data you need to deepen relationships, uncover new opportunities, and advise with confidence.

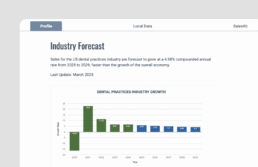

Vertical IQ delivers comprehensive Industry Intelligence with thousands of profiles for every 6-digit NAICS code — covering 100% of the U.S. economy and Canada. From broad sectors to niche markets, each profile offers trusted, data-driven insights to help you prepare, engage, and build stronger client relationships with confidence.

See What We Cover – Search from a sample of our Industry Coverage.

Vertical IQ makes the first appointment feel like the third.Matt Zonno, Senior Vice President & Market Manager, Northwest Bank

Vertical IQ is one of the most powerful tools sales professionals can use to start more conversations with their prospects, clients, and COIs! Brynne Tillman, CEO | LinkedIn Author | LinkedIn Sales Trainer | Sales Navigator Trainer Social Sales Link

Vertical IQ provides me a leading edge to be able to build trust with the client, to be able to gain knowledge with the client that they didn’t really know that I had going into it. And it helps create a client from day one that can last throughout my career.Walt Parker, Business Development Officer

Industry Intelligence plays a big part in training our branch managers and helping them prepare for business appointments. We saw value immediately when an associate on-boarded a valuable new relationship to the bank using Vertical IQ just weeks after training.Michael Torrielli

First Vice President, North Regional Manager,

Cambridge Savings Bank

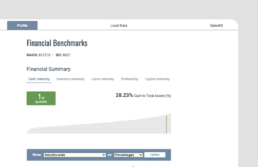

I was calling on a well-known restaurant and hotel investor in California. I knew that he was working with a major hotel chain, so I began sending him Vertical IQ’s Quarterly Emails. Since he already had a lot of experience in the hotel industry, he didn’t immediately see the value of these emails. However, as I persisted, the investor’s target market started to expand, and he began to see the value. He was able to use the “Financial Benchmarks” knowledge in negotiations and saw great success. The investor promised that because of my help, any new hotel purchase would be financed through me.Susan Mackey, Vice President Relationship Manager, Banner Bank

Vertical IQ helps us deliver greater value to our business customers by reducing time spent navigating through the clutter we often encounter when researching business trends and characteristics — we’re more effective in the field which equates to greater mutual success.Lori Dufficy, Director of Sales and Service, Chelsea Groton Bank

Showcase Industry Research Expertise with Business Owners

Download our Free eBook to discover 15 actionable business strategies for building credibility and delivering valuable insights to your clients.

Be more confident.

Speak your client’s language.

Engage and win more clients.

Retain clients longer.

Enrich your sales enablement tools.

Grow your business faster.

Free Trial

Start your 7-day free trial today!

Please enter your personal details to start the process

for a free trial to Business Pro.