Bank CFOs and Chief Credit Officers Can Strengthen CECL Practices With Industry Intelligence

Guest post by Matthew Ashworth, cofounder and managing director of Hyperion Risk…

Smarter Loan Review and Portfolio Monitoring with Industry Research

Guest post by Matthew Ashworth, cofounder and managing director of Hyperion Risk…

Tomorrow’s Trends Today: The Key Economic Drivers Behind Vertical IQ’s Industry Forecasts

What if you could forecast industry trends with the same confidence that a…

Vertical IQ & Lumos Data Empowers Lenders with Insights

Harnessing the Power of Industry Intelligence and SBA Performance Data In…

Unlock Sales Readiness Highlight: Michelle Carpenter, Dart Bank

In our recent ebook, Unlock Sales Readiness: Advice from the Experts, Banking…

Unlock Sales Readiness Highlight: Kenneth Bostwick, Jr., Lakeland Bank

In our recent ebook, Unlock Sales Readiness: Advice from the Experts, Banking…

Vertical IQ Gives Bankers “The Right Stuff” to Save Time & Effort

A high-performing bank has bankers who understand both credit and industry-specific…

Unlock Sales Readiness Highlight: Carol Sexton, Cambridge Savings

In our recent ebook, Unlock Sales Readiness: Advice from the Experts, Banking…

Relationships Built on Trust and Expertise: A Conversation with Business Banking Thought Leader Leslie Parnell

Having served in various banking leadership roles for nearly 20 years, Leslie…

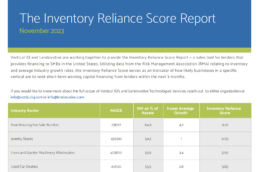

Industries Likely to Need Working Capital Financing in 2024

Vertical IQ and Lendovative Technologies are proud to offer the AR and Inventory…

Identifying the Top Industries for Inventory and AR Financing in 2024

The SBA Office of Advocacy reports that 2.5 million new business formations…

Relational Accounting: Your Competitive Edge in a Data-Driven World

The following is a guest blog post by Amy Vetter, the CEO of B³ Method Institue,…

The Essential Calculation that Must Go into a Cash Flow Analysis

There are many topics about which a strong commercial or corporate analyst should…

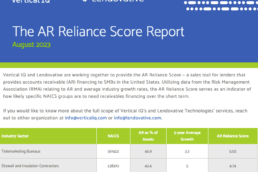

New AR Reliance Score Helps Predict Industries’ Short-Term Financing Needs

The following is a guest blog post by Pat True, the president of Lendovative…

Why I Created Local Market Monitor

Ingo Winzer is the founder of Local Market Monitor, a Vertical IQ product, which…

Attracting More Deposits: Ain’t You Special… Yet?

Vertical IQ co-founder and Clarity Advantage president Nick Miller has been…

First-Hand Account: How Readiness Wins in a Competitive Market

In this guest post, Jerry Bazata, a commercial lender in Portsmouth, New…

After PPP Ends, Don’t Overlook This Important Fourth “P”

By HD Jacobs, Senior Depository and Lending Solutions Product Specialist at S&P…

Potential Benefits and Downsides to Bank and Borrower

Guest post by David Nicholson, Owner of Credit Training Inc.

S&P Global Integrates Vertical IQ Industry Data to Help Lenders Better Understand Customers

By Guest Blogger Cam Saucier, Product Manager, U.S. Financial Institutions at…